.png?width=300&name=CSH%20Logo_Stacked%20400x400%20(2).png)

Is a cost segregation study right for you?

In the end-of-year crunch to find additional cash, is it time to see if you can recover your capital investment sooner? Virtually every taxpayer who owns, constructs, renovates or acquires a real estate facility stands to benefit from a cost segregation study. Our FAQs can help you determine whether a cost segregation study is right for your organization.

Cost Segregation: Frequently Asked Questions

As if another year of the COVID-19 pandemic wasn’t enough to produce an unusual landscape for year-end tax planning, Congress continues to negotiate the budget reconciliation bill. The proposed Build Back Better Act (BBBA) is certain to include some significant tax provisions, but much uncertainty remains about their impact. While we wait to see which tax provisions are ultimately included in the BBBA, here are some year-end tax planning strategies to consider to reduce your 2021 tax liability.

Accelerate and defer with care

One of the most reliable year-end tactics for reducing taxes has long been to accelerate your deductible expenses and defer your income. For example, self-employed individuals who use cash-basis accounting can delay invoices until late December and move up the planned purchase of equipment or the payment of estimated state income taxes from early next year to this year.

This technique has always carried the caveat that you generally shouldn’t pursue it if you expect to be in a higher tax bracket the following year. Potential provisions in the BBBA also may make it advisable for certain taxpayers to reverse the strategy for 2021 — that is, accelerate income and defer deductible expenses.

The current version of the BBBA would impose a new “surtax” of 5% on modified adjusted gross income (MAGI) that exceeds $10 million, with an additional 3% on income of more than $25 million. As a result, the highest earners could pay a 45% federal marginal income tax on wages and business income (the current 37% income tax rate plus 8%). It could be even higher when combined with the net investment income tax, which might be expanded to include active business income for pass-through entities.

In addition, there’s a proposal to temporarily increase the $10,000 cap on the state and local tax deduction to $80,000. Individuals in high-tax states should consider whether there may be an advantage to accelerating a 2022 property or estimated state income tax payment into 2021, or whether the deduction might be more valuable next year, particularly if they’ll face a higher effective tax rate.

Leverage your losses

Taxpayers with substantial capital gains in 2021 could benefit from “harvesting” their losses before year-end. Capital losses can be used to offset capital gains, and up to $3,000 ($1,500 for married persons filing separately) of excess losses (those that exceed the amount of gains for the year) can be applied against ordinary income. Any remaining losses can be carried forward indefinitely.

Beware, however, of the wash-sale rule. Generally, the rule prohibits the deduction of a loss if you acquire “substantially identical” investments within 30 days, before or after, of the date of the sale.

Taxpayers who itemize their deductions could compound their tax benefits by donating the proceeds from the sale of a depreciated investment to a charity. They can both offset realized gains and claim a charitable contribution deduction for the donation.

Satisfy your charitable inclinations

For 2021, charitable contributions can reduce taxes for both itemizers and non-itemizers. Taxpayers who take the standard deduction can claim an above-the-line deduction of $300 ($600 for married couples filing jointly) for cash contributions to qualified charitable organizations.

The adjusted gross income limit for cash donations is 100% for 2021; it’s scheduled to return to 60% for 2022. That means you could offset all of your taxable income with charitable contributions this year. (Donations to donor-advised funds and private foundations don’t qualify, though.)

Taxpayers who don’t generally itemize can benefit by “bunching” their charitable contributions. In other words, delaying or accelerating contributions into a tax year to exceed the standard deduction and claim itemized deductions. For example, if you usually make your donations at the end of the year, you could bunch donations in alternative years — say, donate in January and December of 2022 and January and December of 2024.

Retired taxpayers who are age 70½ and older can reduce their taxable income by making qualified charitable contributions of up to $100,000 from their non-Roth IRAs. Retired or not, individuals age 72 and older can use such contributions to satisfy their annual required minimum distributions (RMDs). Note that RMDs were suspended for 2020 but are effective for 2021.

So long as the assets would be considered long-term if they were sold, donations of appreciated assets offer a double-barreled tax benefit. You avoid the capital gains tax on the appreciation and can deduct the asset’s fair market value as of the date of the gift.

Convert traditional IRAs to Roth IRAs

As in 2020, when many taxpayers saw lower than typical income, 2021 could be a smart time to convert funds in traditional pre-tax IRAs to an after-tax Roth IRA. Roth IRAs have no RMDs, and distributions are tax-free.

You’ll have to pay income tax on the converted funds, but it’s better to do so while subject to lower tax rates. Similarly, if you convert securities that have dropped in value, your tax may well be lower now than down the road — and any subsequent appreciation while in the Roth IRA will be tax-free.

It’s worth noting that President Biden had proposed including a provision in the BBBA that would limit the ability of wealthy individuals to engage in Roth conversions. There was a lot of back-and-forth with respect to these provisions, and the latest version of the House bill includes certain restrictions. Whether these provisions will make it past any Senate amendments remains to be seen, but the proposal could be a harbinger of future proposed restrictions.

Proceed with caution

The year-end tax planning strategies outlined above always come with pros and cons, but perhaps never more so than now, when potentially significant tax legislation that would take effect next year is under negotiation. We can help you chart the best course in light of any developments.

All content provided in this article is for informational purposes only. Matters discussed in this article are subject to change. For up-to-date information on this subject please contact a Clark Schaefer Hackett professional. Clark Schaefer Hackett will not be held responsible for any claim, loss, damage or inconvenience caused as a result of any information within these pages or any information accessed through this site.

- Build Back Better Act (BBBA) overview

- Strategies to reduce year-end tax liability:

- Accelerate and defer with care

- Leverage your losses

- Satisfy your charitable inclinations

- Convert traditional IRAs to Roth IRAs

- Proceed with caution

If your company is planning to build, purchase or renovate a building, or has done so in the past several years, a cost segregation study is a powerful tool that may help boost your cash flow and decrease your tax liability. These Frequently Asked Questions (FAQ) were designed to help you determine whether a cost segregation study is right for you.

Q: Who should consider a cost segregation study?

- Companies that are planning to or that have recently constructed or purchased a building

- Companies that have recently renovated a building they already own or lease

Q: What are the benefits of a cost segregation study?

- A rapid and significant uptick in cash flow

- A decrease in your current tax liability

- The ability to defer taxes

- The opportunity to reclaim past depreciation deductions

Q: How does cost segregation work?

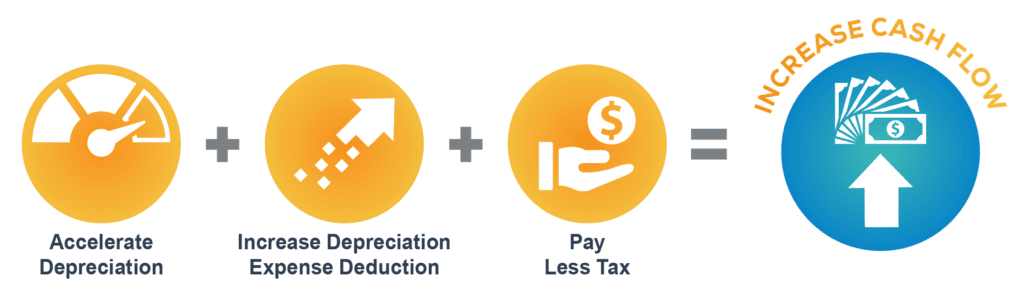

A: Cost segregation is a valuable strategic tax planning tool that separates real property into various depreciable categories, and allows taxpayers to depreciate property over much shorter periods of time than the typical 39-year period.

When you purchase a property, you acquire more than just a structure: you’ve gained a set of building components. While you may look at this as one piece of property, 20% to 40% of the building’s parts and pieces may be looked at differently by the IRS. While structures are normally depreciated over 39 years (27.5 years for residential), it’s possible that some components of your property can be depreciated over 5, 7, or 15 years.

The objective of a cost segregation study is to allocate each of your property-related costs into their appropriate property classes in order to better calculate depreciation deductions. The idea is to analyze – and suitably separate – what’s part of the building, and what’s part of your business.

Q: How does tax reform impact cost segregation?

A: Under the new law, additional depreciation is available for property components that are assigned a depreciation life of 20 years or less. This “bonus depreciation” is now available on both new construction and acquired properties at a rate of 100% (up from a rate of 50% under prior law). This change makes cost segregation even more impactful.

Q: What types of items are reclassified in the study?

- Flooring

- Appliances

- Countertops

- Signage

- Lighting

- Cabinetry

- Landscaping

- Sidewalks

- Parking lots

Note: These are just examples, many types of items can qualify.

Q: What types of properties qualify?

- Office buildings

- Retail centers

- Banks

- Apartment buildings

- Manufacturing facilities (heavy or light)

- Restaurants

- Hotels/motels

- Grocery stores

- Auto dealerships

- Theaters

- Golf courses

- Research and development centers

Note: These are just examples, many types of items can qualify.

Q: I purchased (or constructed) a new building a few years ago, can I still benefit?

A: Yes. You are able to perform cost segregation studies on buildings purchased, built, or improved in prior years. That’s because current IRS rules allow you to “catch up” the additional depreciation in the current tax year, and there’s no need to amend tax returns. In fact, you could see current-year tax benefits from real estate transactions that took place ten or more years ago depending on the size and purchase price of the building.

Q: Isn’t it just timing? Won’t my building depreciate anyway?

A: While it is true that your building will depreciate anyway, a cost segregation study can significantly increase your cash flow in the short term, and provides long-term benefits due to the time value of money (a dollar is worth much more to your business today than it will be in 39 years). Check out our case study for a demonstration of the benefits of a cost segregation study.

Q: How long does a cost segregation study take?

A: Typically, 30-60 days. The timing is often based on the size of the project and whether all of the information and documents are provided upfront.

Q: What documents are needed?

- Architectural drawings

- Construction contract

- Construction budget for the project (if not included with the contract)

- Contractor’s payment applications throughout the project

- Change orders

- Contractor’s final application for payment

- Final project costs

These documents are typically gathered, but a study can still be performed if a client can’t find (or doesn’t have) all of them. Also, the documents listed are only for construction projects. For building acquisitions, we would gather the closing statement, site survey and architectural drawings (if available), appraisal and tenant list.

Q: How much is cost segregation study? What is the ROI? myself?

A: The cost and ROI of a cost segregation study will vary depending on the size of the property, building type, and other physical characteristics. Fees typically range from $5,000 to $15,000 to complete a study, and our clients have realized an average ROI of 54 to 1. That’s right, if a cost segregation study costs a company $10,000 to conduct, they would likely realize a net present value benefit of $540,000 (depending on property type and purchase price).

Q: Can’t I do a study myself? Why do I need to work with a firm that specializes in conducting cost segregation studies?

A: The IRS requires engineering-based cost segregation studies. Your study should be conducted by a firm that demonstrates expertise in engineering, construction, tax law and accounting principles. Clark Schaefer Hackett’s cost segregation practice is led by Brendan Walsh, a licensed attorney and Certified Cost Segregation Professional (CCSP), who has more than 10 years of experience in cost segregation. Brendan is one of only three individuals in the State of Ohio credentialed by the American Society of Cost Segregation Professionals. Nationally, Brendan is one of only 32 CCSPs.

All content provided in this article is for informational purposes only. Matters discussed in this article are subject to change. For up-to-date information on this subject please contact a Clark Schaefer Hackett professional. Clark Schaefer Hackett will not be held responsible for any claim, loss, damage or inconvenience caused as a result of any information within these pages or any information accessed through this site.